RAPT Stock Soars 65% as GSK Makes Bold $2.2B Bet on Food Allergy Future

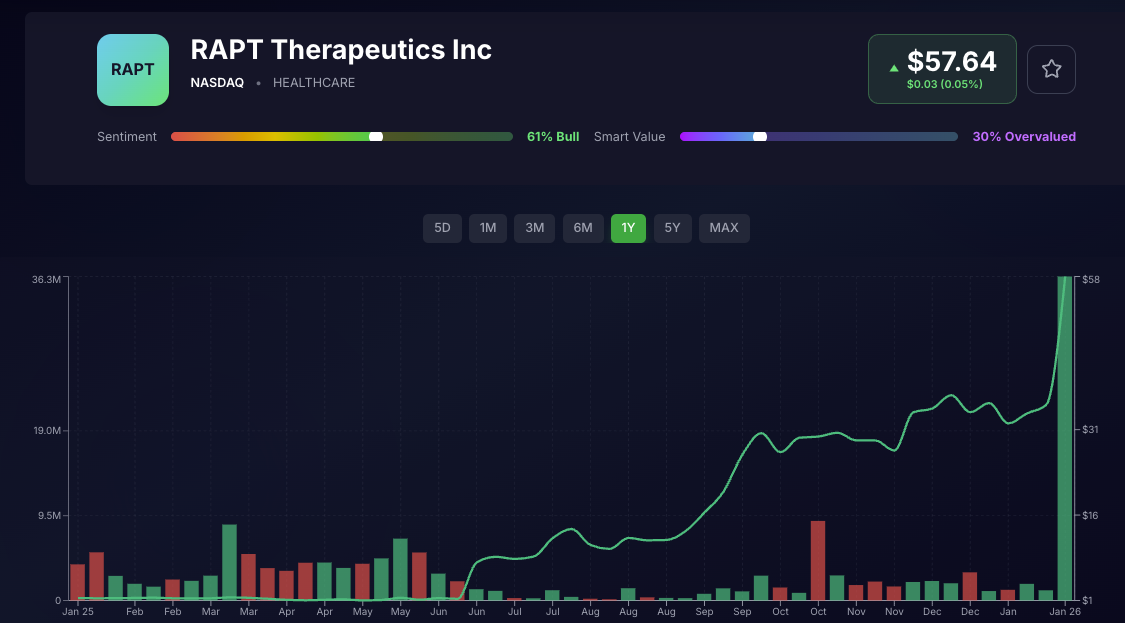

Rapt Therapeutics stock jumped 65% to $57.64 after GSK announced a $2.2 billion acquisition. The deal gives GSK access to ozureprubart, a promising food allergy treatment, as the pharma giant faces a looming patent cliff on its HIV blockbuster dolutegravir.

Key Takeaways

- RAPT stock surged 65% to $57.64 on GSK's $2.2B acquisition at $58/share.

- Ozureprubart targets $15B food allergy market with 12-week dosing vs Xolair's 2-4 weeks.

- GSK faces dolutegravir patent cliff in 2028 losing 20% revenue ($5B+ annually).

Rapt Therapeutics (NASDAQ: RAPT) investors woke up to a massive payday this week. The biotech stock jumped 65% to $57.64 after British pharmaceutical giant GSK announced it's buying the company for $2.2 billion. At $58 per share, it's exactly the kind of premium that makes you wonder if you should have bought RAPT last week.

But this deal is about way more than just a nice exit for RAPT shareholders. It tells us something important about where Big Pharma sees the next decade of growth, and why GSK's new CEO is willing to write a multibillion-dollar check for a drug that won't even have Phase IIb data until 2027.

Why GSK Is Going All-In on Food Allergies

GSK isn't making this acquisition from a position of strength. The company is staring down a brutal reality: its HIV blockbuster dolutegravir, which generated over $5 billion in sales last year, loses patent protection starting in 2028. That's about 20% of GSK's revenue potentially walking out the door over the next few years.

New CEO Luke Miels took the reins just weeks ago, and this RAPT deal is his first major move. The timing isn't coincidental. GSK needs pipeline wins fast, and the pharmaceutical sector has been desperately hunting for growth opportunities in specialty markets where competition is still manageable.

Food allergies fit that bill perfectly. More than 17 million Americans deal with food allergies, leading to over 3 million hospital and emergency room visits annually. The treatment market is projected to grow from $7.5 billion in 2025 to over $15 billion by 2034, according to multiple market research firms. That's nearly 8.5% annual growth in a space that's still relatively uncrowded.

The Drug That's Worth $2.2 Billion

GSK is paying big money for ozureprubart, RAPT's experimental anti-IgE monoclonal antibody designed to prevent allergic reactions to foods like peanuts, milk, eggs, cashews, and walnuts. About 94% of severe food allergies are triggered by IgE-mediated reactions, making this a validated target with proven clinical potential.

What makes ozureprubart interesting is the dosing schedule. Current standard of care requires injections every two to four weeks. RAPT's drug is being tested with 12-week dosing intervals. For parents managing kids with severe food allergies, that's the difference between a clinic visit every month versus once per quarter. Patient compliance matters, especially in pediatrics, and less frequent dosing could be a genuine competitive advantage.

The drug is currently in Phase IIb trials, evaluating patients aged 12 to 55. Results are expected in 2027, with Phase III trials planned for both adult and pediatric populations after that. So we're talking about a drug that's realistically three to four years away from potential FDA approval.

Competing Against Xolair's $2.8 Billion Franchise

GSK knows exactly what it's getting into. Genentech's Xolair (omalizumab) already owns this space, pulling in around $2.8 billion in the first nine months of 2025 across all its indications. The FDA approved Xolair for food allergies in February 2024, making it the first medication specifically authorized to reduce allergic reactions from multiple foods.

That head start is significant. But GSK is betting that better dosing convenience, later-stage pipeline assets, and its established relationships with allergy specialists can carve out meaningful market share. The company recently won FDA approval for a twice-yearly asthma drug, signaling it's building a portfolio of long-acting treatments that reduce the burden on patients and caregivers.

Analysts at Barclays noted that ozureprubart is earlier-stage than they expected GSK to target given the urgency around the dolutegravir patent cliff. Some investors clearly hoped for a "bigger or more transformational" deal from Miels. But GSK's Chief Scientific Officer Tony Wood defended the acquisition, emphasizing that ozureprubart addresses a validated target with clear unmet medical need.

What This Means for Biotech Investors

The RAPT acquisition reflects a broader trend in pharma M&A. With major patent cliffs looming across the industry, Big Pharma companies are paying substantial premiums for assets that won't deliver revenue for years. They're essentially buying time and options, betting that a promising mid-stage pipeline candidate is worth more inside their development machine than it would be as an independent biotech.

For retail investors, deals like this create interesting dynamics. RAPT shareholders got paid handsomely, but they're also giving up exposure to potential upside if ozureprubart becomes a blockbuster. At the same time, GSK shareholders are taking on significant development risk with a drug that's still years away from commercialization.

The stock market seemed split on the deal. RAPT shares traded just under the $58 offer price, suggesting investors believe the deal will close without issues. Meanwhile, GSK shares dropped about 1.6% in London trading as some shareholders questioned whether $2.2 billion was too rich for an unproven asset.

The Bigger Picture

This acquisition shows how desperate major pharmaceutical companies have become to replace revenue that's evaporating as patents expire. The industry is projected to lose over $230 billion to the U.S. market between 2025 and 2030 as blockbuster drugs lose exclusivity. That kind of erosion forces companies to make aggressive bets on earlier-stage assets, even when the risk-reward math looks questionable.

For GSK specifically, the deal makes strategic sense even if it doesn't solve the dolutegravir problem overnight. The company is targeting over $48 billion in risk-adjusted sales by 2031, and it needs at least 12 major product launches to hit that number. Ozureprubart could eventually contribute $2 billion or more in peak annual sales if everything goes right, but that's a big "if" that depends on clinical trial success, regulatory approval, and commercial execution.

The food allergy market offers one clear advantage though: it's not saturated yet. Unlike competitive spaces with five or six established treatments fighting for share, this category still has room for multiple winners. Parents and patients dealing with life-threatening food allergies want options, and doctors will prescribe multiple therapies if they improve outcomes.

RAPT shareholders are celebrating today, but the real test for GSK comes over the next three years. Can ozureprubart deliver strong Phase IIb and Phase III data? Can GSK commercialize it effectively against Xolair? And most importantly, can deals like this fill the revenue gap that's coming as dolutegravir loses patent protection?

Those answers will determine whether Luke Miels' first big move as CEO was brilliant or expensive.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Stock investing involves significant risk, including potential loss of principal. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Recent Articles(9)

View AllWho Is Buying SpaceX at a $1.7 Trillion Valuation?

SpaceX is about to complete the largest IPO in history at a $1.7 trillion valuation, but a sum-of-the-parts analysis puts the company's intrinsic value closer to $350 to $780 billion. Here's why Starlink carries the entire business, why the price is really an AI bet, and what value investors should make of it.

NVTS Forecast 2030: Why Navitas Semiconductor Could Hit $500M (Or More)

Navitas Semiconductor (NVTS) generated $45.9 million in 2025 revenue while management targets a $3.5 billion serviceable market by 2030. Here's a probability-weighted look at where NVTS annual revenue could actually land in 2030, and why the stock has rallied nearly 1,000% in a year.

Will NVIDIA Stock Hit $300 in 2026? A Probability-Weighted Forecast

Can NVIDIA stock reach $300 by end of 2026? Three Wall Street banks say yes, with BofA at $320 and Tigress at $360. Here's the probability-weighted breakdown ahead of NVDA's Q1 FY2027 earnings on May 20.

Trump Just Disclosed Up to $750M in Q1 Stock Trades. The AI Infrastructure Pattern Is Hard to Ignore

President Trump disclosed more than 3,700 securities transactions worth up to $750 million in Q1 2026, with several buys landing one to two weeks before favorable regulatory decisions in those exact names. Here's what the AI infrastructure pattern signals for retail investors and where the second-derivative trade lives.

How to Track Smart Money: A Free Tool for Following Institutional Investors

Track 67 of the most-followed institutional investors managing $1.11 trillion in equities through SEC 13F filings. Our new free Superinvestor Tracker lets retail investors compare hedge fund and asset manager portfolios side by side without paying for a Bloomberg terminal.

Which Stock Will Be the First $6 Trillion Company?

Nvidia just closed at a $5.05 trillion market cap. Alphabet is hot on its heels at $4.80 trillion. The race to be the first $6 trillion company is closer than most retail investors realize, but the math still favors one name. Here is the realistic breakdown of who gets there first in 2026 and why.

RAM Prices Are Exploding: Inside the Great Memory Squeeze Wall Street Underestimated

DRAM contract prices surged 55-60% QoQ as AI demand permanently rewired the global memory market. Here are the top 10 memory makers by market share, which stocks win from the supercycle, and why server OEMs like Dell and HP are getting margin-crushed.

CoreWeave Just Locked In Meta and Anthropic in 48 Hours. Is CRWV a Buy in 2026?

CoreWeave locked in $21B from Meta and a multi-year Anthropic deal in 48 hours, pushing backlog to $87.8B. Is CRWV stock a buy in 2026? Here is the probability-weighted take.

How the Iran War Quietly Became the Biggest Threat to AI Infrastructure Stocks

The Iran war wasn't just an oil story, it was a stress test for AI infrastructure stocks. Here's how IREN, CoreWeave, Nebius, and Nvidia are really exposed to energy cost shocks, and which names look best positioned after the ceasefire.

About WSS Team

WallStSmart editorial team delivering professional financial analysis and market insights.

Follow on Twitter